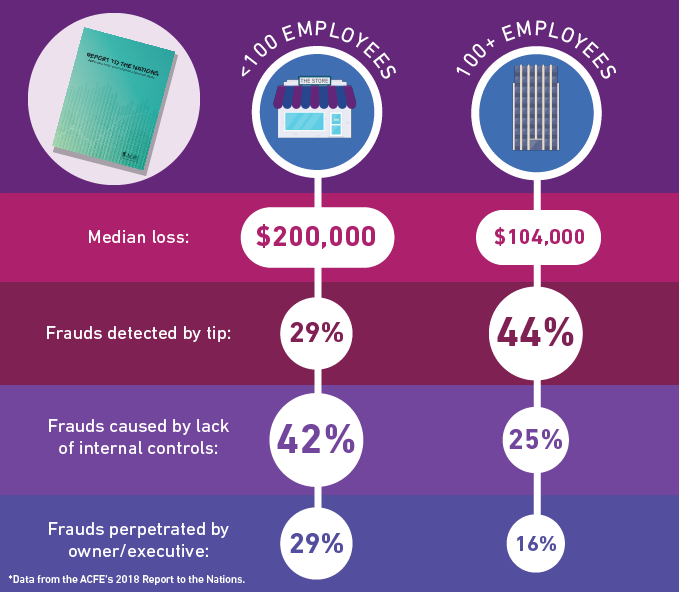

Fraud is a sad reality of our modern society. According to the Association of Certified Fraud Examiners (ACFE), small businesses and private companies drive 42% of fraud incidents.

The impact of fraud hits your organization in various ways, including reputational damage and monetary losses.

According to the same study referenced above, US businesses lose an average of 5% of their annual revenue to fraudulent activities.

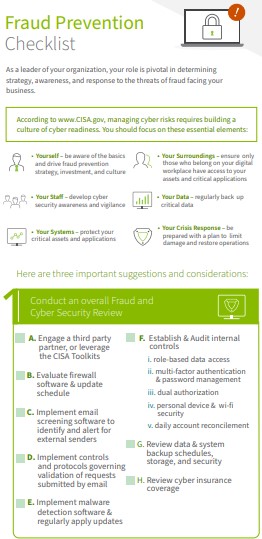

The best way to protect yourself against fraudsters is through prevention. Make sure your business has appropriate internal controls, implements proper employee training, and conducts internal audits.

Let’s take a closer look at managing fraud risk and saving your business from irreversible damage.

Recognize that fraud can occur in any business

Fraud is a serious issue that can happen anywhere, at any time.

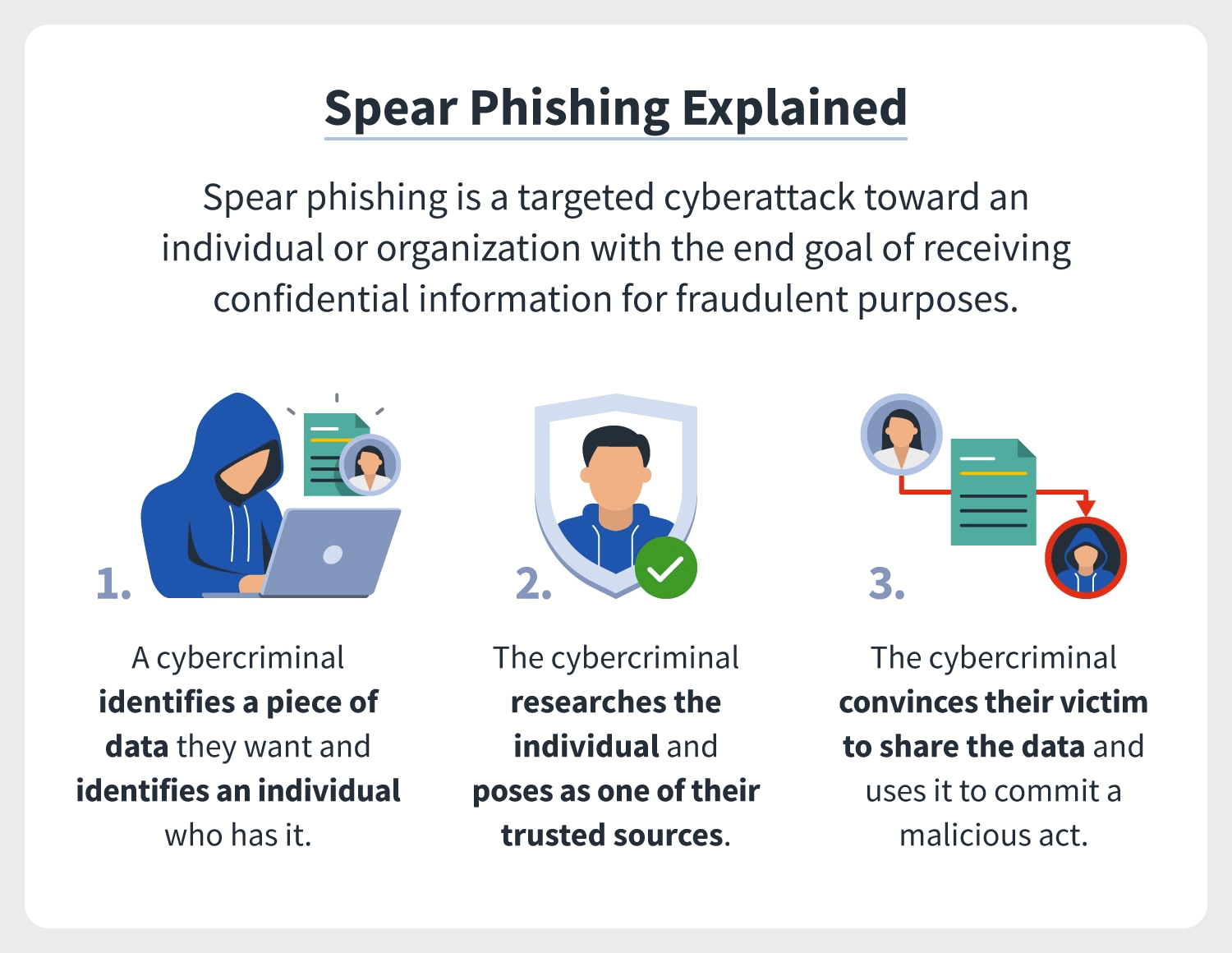

And it isn’t just your employees who might commit fraud. You may be the victim of suppliers and other external stakeholders attempting to exploit your weaknesses. An employee interacting with an email marketing message in their inbox could turn out to be a spear phishing attack on your company.

As a business owner or manager, stop the risk of fraud by implementing controls. Train employees to recognize red flags.

Don’t assume you can spot a fraudster based on a physical appearance

Fraudsters come in all shapes and sizes. They don’t have any specific physical appearance or personality traits you can use as a red flag.

While you may rely on your employees to never steal from you, bad actors can be very good at blending in.

Fraudsters are often very clever when committing these acts — quick-thinkers who adapt when things go wrong. Additionally, because they’re good at what they do (fraud), many people (you and your security team) may not even realize something’s wrong until it’s too late.

Your organization must look out for potential signs of fraud and develop skills to identify possible threats before they happen.

Understand the different types of fraud

When planning an effective fraud risk management strategy, you must know what type of fraud you’re likely to encounter. Here are some of the most common types:

- Financial fraud (e.g., embezzlement)

- Insider fraud (e.g., hacking or theft)

- Accounting fraud (e.g., manipulating financial statements)

- Bribery and corruption (e.g., bribes from customers or vendors)

- Fraudulent procurement (e.g., purchasing counterfeit goods)

- Fraudulent billing (e.g., paying for services that aren’t delivered)

- Fraudulent insurance (e.g., filing false claims against an insurance policy)

Build a corporate culture of honesty, transparency, and accountability

Fraud risk is preventable by creating a corporate culture of honesty, transparency, and accountability.

All employees must operate with integrity if you want your company to minimize its exposure to fraud. This means having clear boundaries for acceptable behavior within your organization and enforcing those rules consistently for everyone in the workplace — from CEOs down through the ranks.

Centralize your data and enhance controls

Data is everywhere. Your company probably has a lot of it, and it’s not just the data you’re actively using — it’s also the data you’ve accumulated over time.

Access to sensitive data is a common desire for fraudsters. It’s crucial to increase the security around your data.

- Centralize your data: If there are multiple locations where sensitive information exists (like on different servers or hard drives), merge it into one data center. Invest in data center infrastructure management software to increase security and lower operating costs if you house large amounts of sensitive information.

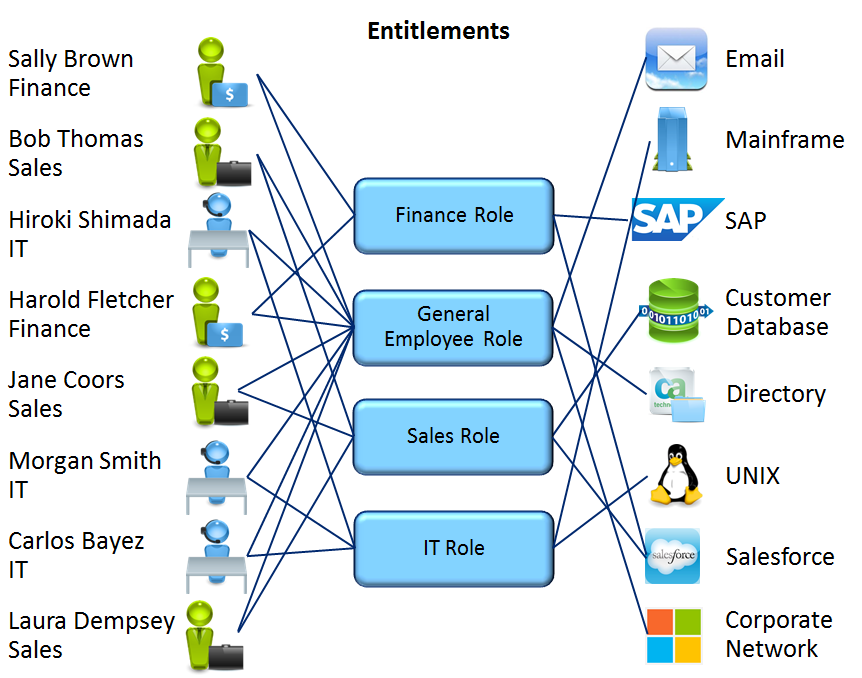

- Control access and entitlements: Limit access to sensitive data based on job function or rank within your organization. Sometimes, less is more.

Additionally, use a reliable password manager instead of saving it on a sticky note on your desktop or, worse, a compromised file document. Password management tools can help protect your business’s online identity.

Implement proper controls for high-risk activities

While it may seem obvious to put controls in place for transactions involving high-risk activities, this is an often overlooked step. To combat this, you should:

- Know who’s involved in the transaction

- Know the purpose of each transaction

- Track the frequency and urgency of transactions

Continue to evaluate, test, and implement controls regularly. Remember, don’t stop once these controls are in place. This process involves:

- Evaluating your existing controls

- Identifying any gaps

- Implementing new technology and controls

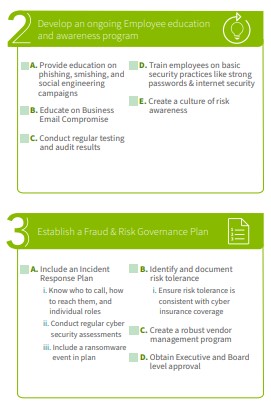

Provide fraud risk training for your employees

You can’t expect your employees to catch fraud if they don’t know what it looks like. Fraud training is essential for everyone on your team and should adhere to the specific risks that apply to your business. Through fraud risk assessment and training, employees will learn to spot red flags and point them out before they escalate into more significant problems.

Here are some ways you can train your employees:

- Provide regular training sessions so that they know how to identify common types of fraud.

- Hold an annual training session where staff members review best practices and discuss any new issues that have come up since last year’s session took place.

- Offer an internal fraud risk portal where employees can read educational materials or submit a potential fraud alert with no questions asked.

All businesses need to have a team-based approach to preventing fraud. Every person involved in day-to-day operations should know the signs of fraudulent activity so that when something seems off, they can flag it immediately without hesitation or fear of being too cautious. You can never be too careful regarding fraud risk and prevention.

Wrapping up

Fraud is a serious issue affecting businesses of all sizes and across all industries.

Skipping out on fraud prevention is no longer an option. As a business owner or decision-maker, you’re legally responsible for protecting your organization from fraud. If you ever decide to sell your business, you must prove to the buyer that you are running a secure operation. No one wants to buy a company that could be at high risk of fraudulent activity.

The best way to protect your company from fraud is by having robust internal controls that keep employees accountable and make detecting fraud easy.

Despite these measures, you still need to be vigilant about identifying when something might go wrong. Keep an eye on unusual or suspicious activity within your organization and conduct regular audits to ensure you aren’t missing any red flags.